Founder-led companies are reshaping global equity markets. Our 2026 Annual Report examines why companies shaped by founders have outperformed over the past decade, grown into a larger share of global market capitalisation, and become an increasingly important force for investors to understand.

This article is Part 3 of a three-part series about Graham Turner, Founder of Flight Centre.

***

Applying Evolutionary Psychology to Corporate Culture

Conventional corporate structure is made of a hierarchical, pyramid structure which Skroo does not ascribe to. The reason is because it slows decision-making, adds bureaucratic layers and disrupts the flow of customer feedback back up to management. The secret formula Flight Centre employed during their rapid pace was based on the theory of evolutionary psychology written by Professor Nigel Nicholson from London School of Economics. The design of an organisation is centred around teams of 5 to 8 people which hark back to how our hunter gatherer ancestors liked to live and work as a family. Typically 5 to 8 families make a village (an informal group that helps and works with each other), and 3 to 8 villages make a tribe. A tribe ideally consists of 80-150 people. Any larger unnecessary bureaucracy starts to creep in.

On organisational design: “You can take people from the Stone Age, but you can’t take the Stone Age out of people” – Graham Turner

This is how Skroo designed Flight Centre’s frontline teams – roughly 5 to 8 team members in any new shop, belonging to a village of 5 to 8 shops, which in turn linked to a tribe consisting of about 3 to 5 villages (15 to 25 shops). The ideal tribe had around 150 people. As Flight Centre grew beyond those limits, it had to inevitably embrace a level of bureaucracy which Skroo minimised by limiting it to a maximum of 3 or 4 levels – team level, followed by tribe level, then region level, then country level. Senior management should be a maximum of 4 or 5 levels away from frontline staff.

Organisational Structure In the Context of Evolutionary Psychology

To this day Flight Centre is structured this way and Skroo remains adamant the size of its board and senior management team should be no different than a family – a maximum of 5 to 8.

How To Acquire Companies

Skroo has overseen a 20 year track record of acquisitions and proudly stands by the fact he’s made plenty of mistakes. He is the first to admit a success rate of “50/50” is not impressive, but the courage of continuing to take risks is part of why Flight Centre has been successful. It is the reason that has enabled its longstanding leadership team to finetune its acquisition criteria and continue learning from mistakes.

For starters, he eschews “renovators” where on balance more time and capital is required than one estimates. He instead prefers ready-made targets that can already contribute immediately. The premium on acquiring these companies is worth it. Its biggest successes have come from acquisitions in adjacent markets. For example, Flight Centre was able to move into the corporate travel business through a string of acquisitions; it is now one of its largest business areas.

These days, Flight Centre has significant internal capabilities to grow by itself; it will only look to acquire where there are opportunities in niche markets where it does not already have exposure. That may be in new travel segments (such as leisure) or niche geographies where there are new growth opportunities. And this is the other key lesson Skroo has learnt – acquiring is not about empire building for the sake of organisational size; it is about building an advantage in a new niche.

The Makings of a Founder

To this day Skroo remains the CEO and retains a significant shareholding. Reflecting on his own journey, I ask him the ingredients which made him a successful founder and what separated him from others. In typical Skroo fashion, he responds analytically with a sense of realism: “getting my hands dirty on an apple orchard by the age of six set a foundation for understanding small business. It’s not a requirement for success, but certainly helped me learn the basics.”

As he developed, it became clear he was a builder – 2 buses was never enough. With a dry grin he points out he was motivated to pursue life outside the family’s apple orchard because “it was so boring” and of course he pays heed to a splash of luck which helped him survive the cash crisis early on. Somehow I suspect the element of luck is less than Skroo purports.

***

For our other articles on founders, search ‘Founder interview’ in our Knowledge Bank

This article is Part 2 of a three-part series about Graham Turner, Founder of Flight Centre.

***

Finding a Niche

Founders like Skroo always find a way to reinvent and adapt. Motivated by a return to Australia with his family, he looked to exit Topdeck but still had one eye on his next move. From his time in London, he noticed the travel market in Australia by comparison was relatively homogenous, controlled predominantly by big institutions who were happy selling exorbitant airfares with little competition. Skroo saw this environment as a ripe opportunity to build a niche – discount travel. He would have an edge sourcing flights from overseas airlines looking to offload tickets at the last minute given his connections in London.

The discount airfare retailers, known as bucket shops in London, was a concept not well known to Australia. At the time, airfare discounting was illegal, it was only a few years later that regulations would change and allow the market to open. As Skroo recalls, there were a few discount retailers who were prosecuted, but he was lucky to avoid this and flourish when the regulations were updated. He fondly remembers the deliberately handwriting messy promotions on shopfront blackboards as a tactic to attract the discount bargain hunters.

“Again we got into a niche that meant we could almost have as many customers as we wanted within reason” – Graham Turner

Taking the cash lessons from Topdeck, market entry was conservatively executed, preserving cash through the use of partnerships in the pursuit of an expansion strategy. When Flight Centre opened its first stores in Brisbane, Sydney and Melbourne, it did so via joint venture arrangements which minimised the amount of cash required. From those three domestic shops, they would eventually spread internationally not long after.

Graham Turner and Lawrence Lam

Going Global The Right Way

Global expansion has traditionally been difficult for many Australian companies. It was no different for Flight Centre. The difference maker was at Flight Centre, there was a group of co-founders at the helm determined to figure out and evolve their overseas operations. They also had the ability to make quick changes without heavy bureaucracy many other organisations face.

In 1989 the business opened its first overseas shops in London and California. Despite Skroo’s extensive experience in London, the shops struggled to gain traction. Skroo puts it down to two factors: timing and leadership talent. The expansion overseas was premature because in those days Flight Centre did not yet have the level of buying power it needed to acquire the cheapest possible airfares, meaning it could not offer the competitive pricing it needed to break into a new market. Its leadership talent was also quite thin which meant decision-making was made from afar in Australia; on the ground experience was lacking. The disappointing results led to the eventual closing of the London and Californian shops in 1991.

But unlike large corporates, Skroo’s operation was agile, could make quick decisions, and was determined to make the global expansion work. In 1995 they revisited the plan with a much stronger foundation. By then Flight Centre had just floated and had built up 350 shops in Australia, generating about $1 billion in revenues. With that also came a deeper talent pool of managers with greater skill and affinity to what Flight Centre was about – its corporate culture. The previous constraints which prevented a successful expansion were fixed. As Skroo puts it “this time we didn’t underestimate how difficult it was to start something up like that.”

Instead of hiring leaders overseas, Flight Centre sent, as Skroo put it “really good expats”, from Australia with a horizon of five to ten years to lead and grow the overseas operations. This tweak worked. It highlighted the importance of corporate culture and business acumen, which took years to develop. Eventually the expat would hand over to a local manager. Even today the formula for spotting internal talent has not changed – Skroo looks for those who make the right commercial judgements, reflect the corporate culture and are willing to relocate even with young families – “it is a big commitment and people prepared to make those commitments tells you something”.

It was with this approach that Skroo and his team would successfully expand into the UK and US throughout the 1990’s and would set Flight Centre on the path towards a true multinational business it is today.

***

For our other articles on founders, search ‘Founder interview’ in our Knowledge Bank

Much has been written about Graham Turner’s career and how he grew Flight Centre from a single shop in 1982 to a global enterprise generating $3 billion of revenue in over 80 countries. But not many know about the proverbial mountains he’s climbed to get to where he is today. It is through these many storms that his uncanny business intuition has been honed. In my interview with ‘Skroo’ (as he prefers to be called), we unstitch the fabric of these experiences and the lessons he’s learnt over decades in business.

Graham Turner and Lawrence Lam

Big Businesses Start Small… But Always Differentiated

Introverted, Intuitive, Thinking and Prospecting. This is the combination of descriptors that make up Skroo’s Myer’s-Briggs personality type. In their natural state, INTP types are quiet thinkers with vigorous intellects. They enjoy seeking out unlikely paths and taking an unconventional approach.

It becomes abundantly clear these descriptors fit very well with all that Skroo has overcome in his business journey. It explains why he started a business on the other side of the world ‘just for fun’ with a few mates over 50 years ago.

Just as intriguing as the why, is how he scaled from one bus in 1973 to over seventy by 1980, running tours all over Europe. Skroo tells me the story of how he purchased the first bus and launched Top Deck Travel. At the time bus tour companies were in great abundance throughout London. There was no shortage of competition. But when Skroo and his mates fitted out their first bus, he fitted them with a kitchen and bedrooms, capable of taking long-haul trips as far as Afghanistan. It came simply from the fact they wanted to see more countries on a shoestring budget, but in doing so had inadvertently stumbled across his first business lesson: in competitive markets, a subtle differentiation can open up new pockets of demand. Competitors at the time were focused on coach camping tours, not long-haul tours like Skroo’s bus. What Top Deck offered was unique and fun. Customers could cook, sleep and visit more countries, which made it an attractive and unique proposition.

A Unique Value Proposition

The ease with which seats were filled gave Skroo and his business partner a taste of early success. Although the business concept of blue oceans would be popularised some decades later, Skroo had already discovered the advantages of creating new markets early on through the differentiation of the tour experience. The unit economics were prime for scaling. At a cost of £12 in weekly marketing costs (Skroo tells me the first ads were placed in a weekly travel newspaper published in London called the Australiasian Express), Topdeck could confidently fill a bus which would deliver revenues of £1,650. Even accounting for other expenses, each trip was profoundly profitable.

Scaling became easy with the growing demand and self-generating cashflows. Two years into operations, Topdeck made £15,000 profit and had several buses touring all over Europe. Along the way, he enjoyed many free overland trips, including a 3-month drive from London to Kathmandu. Underneath Skroo’s thoughtful and calm demeanour was a strong desire for growth and success. He still enjoys winning in the game of business. As he says “Founders are generally empire builders. One bus was never enough for me. It had to be 2, 3, or 10.”

But how does a founder balance the investment required to scale, with the cash needs in the short-term? It was a question of balancing long-term growth and short-term liquidity. Initially, they developed a general rule: every bus purchase should only be made if they were confident it could be paid back in 2-3 trips. The model worked well for the first 10 years as they scaled to 70 buses but by 1980 the market changed. Skroo was about to learn his toughest lesson in business when Topdeck almost filed for bankruptcy.

Balancing Liquidity and Scalable Unit Economics

By 1980 Topdeck had seventy buses all over Europe and despite the strong growth trajectory, found itself short of cash when forward bookings in the winter were weaker than expected. And because it had a model that relied on rapid scaling and reinvestment of cash back into more buses, Topdeck became exceptionally reliant on forward bookings. It was the business’s first near death experience and taught Skroo a lesson in cash management. Its importance became abundantly clear as Skroo was turned down by banks who had no interest in financing a bus tour business. There would be no white knights. No one was going to save Topdeck in its most crucial time of need. As Skroo aptly puts it: “banks are more likely to loan money to those that don’t need it”.

They survived by the skin of their teeth only because cash from bookings originating from Australia and New Zealand started flowing through in April of 1980. The southern hemisphere booking season had come through just in time. It was a close call. Survival had come from internal cash, not external. In business there is no such thing as a deus ex machina.

For Skroo, the importance of cash is a recurring lesson he sees over and over again. Forty years on, even after he left the Topdeck business in 1986 and returned to Australia to eventually start Flight Centre, his recollection of that moment is as visceral as ever. That moment shaped how Flight Centre would manage its cash position, and the amount of debt it would hold going forward.

***

For our other articles on founders, search ‘Founder interview’ in our Knowledge Bank

In Part 1 we detailed how Jack Gance and his brother, Sam, built the sunglass and cosmetics distributor Le Specs before selling the business in 1990. The Le Specs business was originally launched as a pharmacist-to-pharmacist wholesaler, and Jack and his brother Sam were themselves qualified pharmacists with their own established pharmacies.

Separate to the Le Specs business, Jack was concurrently cultivating a footprint of pharmacies in Victoria which grew from 2 to 35 through a series of partnerships. This chain of stores would eventually be branded as the MyChemist. It would be the first iteration of what would spark the creation of Chemist Warehouse – the second phase of Jack’s career and his biggest success. It would become a pharmacy brand that would dominate the Australian market.

Jack Gance (right) with author Lawrence Lam

Creating new opportunities in crowded markets

Prior to Chemist Warehouse, the pharmacy market in Australia was fragmented and traditionally hard to scale due to strict regulations and the requirement to have qualified pharmacists on premises. That was until Jack changed the business model.

Traditionally, the local chemist was a member of the community, just like the local doctor. Roughly 70% of revenues of the average pharmacy store were from prescription drugs, and the remaining 30% being from non-prescription drugs and other health-related products.

The Chemist Warehouse model flips this script. Most sales are from non-prescription drugs such as vitamins, fragrances, cosmetics, skincare, and natural medicines. This segment, often referred to as the ‘front-of-shop’ sales, accounts for approximately 70% of revenues, whereas prescription medicines (behind-the-counter) are 30% of revenues. Readers should not misinterpret Chemist Warehouse as generating less prescription sales, but rather it sells far more front-of-shop products than the average pharmacy in Australia. Prescription sales remain on par, if not more, than the average pharmacy.

Chemist Warehouse’s growth comes from the ability to create a new market within an established industry. It does this by increasing the floorspace allocated to front-of-shop products, flipping the traditional drug-focused pharmacy model into a warehouse focused on showcasing all the non-prescription products. Jack’s retail philosophy centres around bombarding customers with such a wide variety of products that they will eventually find something that they want. “If you walk into a shop looking for a tie and the shop has three ties, you might not buy one. But if the shop has 1,000 ties, you’re more likely to find one or more that suit you”, Jack says.

“If you walk into a shop looking for a tie and the shop has three ties, you might not buy one. But if the shop has 1,000 ties, you’re more likely to find one or more that suit you” – Jack Gance

This philosophy also gives the ability to cross-sell more products. Like the Costco model, customers of Chemist Warehouse often walk out buying more than they intended simply because of the overwhelming product range and overt signage which serves as a reminder of all the forgotten shopping list items. On average, the revenue of a Chemist Warehouse store is roughly four to six times that of an average pharmacy store due to the velocity at which they turn over stock. This brings scale and buying power from suppliers which in turn enables low pricing for customers.

From an investment perspective, Chemist Warehouse is akin to a platform business. It’s reputation as the preeminent low-cost pharmacy brand means consumers will gravitate to their shops. They match these consumers with vendors selling cosmetics, vitamins, skincare, and health products. Their ‘platform’ is the network of 500 stores that give them the footprint to be the country’s number one pharmacy retailer.

The physical store network is connected by unified sales systems and inventory management systems which allow head office a centralised view of the platform. Like most platform businesses, they have self-perpetuating monopolistic characteristics as buyers and sellers reinforce the need to transact through Chemist Warehouse. Ultimately this creates scale and reduces inventory risk for Jack’s business. The more they sell, the lower the prices they can offer, and the more customers they win.

A founder’s connection to their business

Many pharmacy retailers have attempted to create a national chain though none have dominated the market like Chemist Warehouse.

From the outset of my interview with Jack, it’s abundantly clear he retains intimate knowledge of the business despite much of the daily operations now being run by his team of 500 at head office. He cites store sales figures from the prior week and tells me which products are trending in his stores. He receives daily reports from the centralised sales and inventory management systems.

What he detests are business leaders detached from their customers. Jack tells me about a conversation he had with the CEO of a leading Australian health company selling a significant amount of product to Chemist Warehouse. Jack asked the freshly appointed CEO, a non-founder, if he knew the name of Chemist Warehouse’s representative buyer – the key influencer who determines which products Chemist Warehouse will buy and in what quantity. The CEO was not able to. Jack asked if the CEO knew the buyer’s name from one of Australia’s largest supermarkets, another key client. “Jack, I know the CEO of the supermarket chain, but I don’t know the buyer by name. I’m a CEO of a multinational business, I have thousands of clients and it’s impossible for me to know every buyer by name”, he said.

But that is the essence of why founder-led businesses are different. As Jack points out, both Chemist Warehouse and the supermarket chain represent a significant portion of this company’s revenues. In his view, a CEO must foster a close relationship with those individuals at the heart of the decision-making process of their customers.

In search of the next Jack Gance

Jack is cautiously aggressive when it comes to business. An example is Chemist Warehouse’s expansion into the New Zealand and Ireland. “Many companies have failed with big overseas expansion plans,” he tells me, reeling off names of Australian companies that have expanded too fast overseas. Although the eventual plan is to expand into the United Kingdom, Chemist Warehouse has opted to test the market in nearby Ireland first by piloting a small number of stores.

“I don’t assume I know more than the local market,” Jack emphasises. He looks to form partnerships with local operators to minimise the learning curve and expansion costs.

Like many founder-led companies, Jack runs Chemist Warehouse with very little debt. The focus has been on positive cashflow generation and long-term financial stability, an awareness he gained from his Le Specs days which was an operation hungry for working capital.

He favours organic growth over large acquisitions. In 2017, Chemist Warehouse expanded into New Zealand with its first stores initially funded with $5 million of starting capital. New Zealand, with its less stringent regulatory framework compared to Australia, has proven a fertile ground for Chemist Warehouse’s expansion. Aside from the initial capital, the expansion has not required additional investment – the new stores continue to be self-funded by revenues from existing New Zealand stores.

With organic opportunities in abundance, very few acquisitions make sense to Jack. Like most long-term minded founders, that is exactly the way he prefers.

Jack’s style errs on self-reliance rather than outsourcing. Early on he chose to run his own centralised sales software system on Chemist Warehouse’s cash registers to centralise the sales data. The vertically integrated model is a core strategic advantage of the business. It gives head office granular visibility over the entire store network and standardises the technology infrastructure, enabling efficiency when rolling out new stores and products.

A lesson on risk taking

Jack believes true entrepreneurs are risk mitigators. He did this with the marketing deal he struck to launch Le Specs, paying no upfront costs, and instead sharing a percentage of subsequent profits, thereby reducing the expenditure outlayed in case the venture was unsuccessful. And Chemist Warehouse’s cautiously aggressive UK expansion plan has Jack’s risk management philosophy written all over it.

Though a success story, Jack has experienced his share of failures. After he sold Le Specs, Jack remained in management for two years, working with the new owner during the transition. He watched Le Tan decline under new ownership as he lost the decision-making power to reverse the trend. He attributes the experience as a lesson in the importance of maintaining good relationships with suppliers, not just customers. When the new owner took over, suppliers were strong-armed into renegotiating contracts with unfavourable terms for them. This proved successful for Le Tan in the short-term but eroded the quality of the product as relationships later deteriorated.

Companies that localise an already proven global model

Smaller niche markets may appear less appealing to investors, but even in the sunglasses and pharmacy market in a relatively small country like Australia, Jack Gance has managed to create significant value. The conventional view teaches investors to focus on markets with a large Total Addressable Market (“TAM”), but with larger TAM comes greater attention and increased competition. Instead, investors may find opportunity in companies that localise products and services that have already been proven to work overseas.

For instance, Le Specs introduced a tougher, more flexible sunglass range that was first manufactured and sold in France. Jack localised it for the Australian market after his wife Evelynne visited a trade show in France.

Similarly, he describes how the idea of Chemist Warehouse came about after having visited the “busy, in-you-face, warehouse-style” pharmacies in the US during the 1970s.

The localisation strategy epitomises Jack’s focus on risk minimisation; adapting a proven model overseas is much less risky than creating an untested one.

***

For our other articles on founders, search ‘Founder interview’ in our Knowledge Bank

Jack Gance is a rare entrepreneur who’s created not one but two dominant market leaders from scratch. He built Australia’s leading pharmacy retailer, Chemist Warehouse, after founding and ultimately selling Le Specs, one of the top brands in fragrances, cosmetics, suntan lotion and sunglasses. Throughout my interview with Jack, he sprinkles lessons in getting businesses off the ground with limited capital, on how to create and extend strategic advantages, building businesses over a long horizon, as well as the importance of making fair deals with suppliers.

Jack Gance (right) with author Lawrence Lam

Getting your foot in the door

Within the opening few minutes of our interview, it becomes apparent Jack chooses to take calculated risks in areas where he has a strategic advantage. ‘What exactly do you define as a strategic advantage?’ I ask. In a matter-of-fact tone, Jack explains it’s about getting yourself into unfair fights.

For example, the Le Specs sunglasses business was launched as a pharmacist-to-pharmacist wholesaler. Jack and his brother Sam were themselves qualified pharmacists with their own established pharmacies. Jack had the insider’s advantage of being a relatable colleague familiar with how pharmacists should position the product. Jack was able to distinguish Le Specs, which had a unique feature of being unbreakable, from the hundreds of other sunglass products and distributors to garner the support of fellow colleagues.

The insider’s angle combined with a unique product proved to be enough of a differentiator to give Jack the leg-up he needed. He knew how to price the sunglasses, and he could coach his sales team on how to maximise sales.

A story he recalls involves a time when he would ask pharmacists to step on the sunglasses to demonstrate why they would appeal to the masses. He would also encourage them to repeat this in front of customers – a way to grab their attention.

Combined with the attractive wholesale prices, Le Specs was an immediate success. And as any founder would, Jack pressed on further with an innovative marketing deal which would propel the brand on a national level.

Getting the first break with limited capital

Jack recalls approaching an advertising agency in 1979 to propose a unique marketing deal (at the time he didn’t have the capital to invest large amounts into advertising). Instead of Le Specs giving the agency a large upfront fee, the agency would receive a percentage of sales. In return they would help brand, launch and create the advertising for the product. Jack won them over by ‘throwing the sunglasses on the ground and stepping on them’ – to demonstrate the uniqueness of the product.

The deal incentivised the advertising agency and it went above and beyond to promote the product, finding extra TV marketing slots for Le Specs that otherwise would not have been filled. A year later, Le Specs expanded nationally, having established itself as the market leader in tough and affordable sunglasses.

The marketing deal allowed Jack to limit his initial capital outlay, de-risk the venture and create an incentive structure with the advertising agency that would allow Le Specs to gain national brand recognition.

By the time competitors started entering a year later, Le Specs had already established a substantial lead in market share and support from customers. As Jack says, ‘the advertising deal gave us the break we needed to kickstart our operations’.

Minimise initial risk and capital outlay, gain a foothold and expand your strategic advantage over time – this is the modus operandi that would resonate through Jack’s career.

Expanding your strategic advantage

As more competitors entered the market, Jack had to secure exclusive distribution agreements from the French manufacturer. On one trip, he flew to Lyon to meet the manufacturer to convince them he should be the sole distributor in Australia of its unbreakable sunglasses. Exclusivity helped to temporarily prolong Le Specs’ first mover advantage, crucial in the early stages of the business. Over time, more manufacturers appeared but Jack could only secure exclusivity deals with so many. He could see Le Spec’s strategic advantage was under the microscope of its competitors, soon to be studied, dissected, and replicated. But Jack had other ideas to broaden his business. He was already thinking about the next horizon – In his mind the key question was:

Is Le Specs a sunglasses business, or is it a distribution business?

With the leading brand name and national sales channels, Jack saw Le Specs as a distribution business first, which just so happened to sell sunglasses. And with this conclusion, the way he needed to expand his strategic foothold was to sell another product to his customers.

It was Jack’s intention to diversify into a winter-orientated product to balance out the summer-heavy sales of sunglasses, but he struggled to think of any promising ideas. Instead of taking a dogmatic approach, Jack went with developing another summer product – suntan lotion. Yes, it meant his sales profile was heavily tied to the summer season, but suntan lotion had the advantage of being an easier sell. Jack’s orchestrated sales process made sure every salesperson pitched a bottle of suntan lotion at the same time they sold a pair of sunglasses. The lotion was branded Le Tan, designed to ride off the positive branding of Le Specs. It worked. Sales grew organically as the product range expanded.

With the self-clarity of knowing he was running a distribution business, not a sunglasses or suntan lotion business, there was an impetus to keep rolling out new products. The next idea was the perfume market, which was a much larger market and traditionally sold through department stores, not pharmacies.

This led to the acquisition of Australis, a brand which had historically struggled to grow. The reason, in Jack’s view, was because Australis’s branding was competing head on with fragrance brands like Chanel and Dior. The branding was too serious; Australis would always lose in a battle for sophistication. Instead, Jack emphasised the need for products to create a ‘smile factor’ – he was going to counter the strategic advantage (and million-dollar marketing budgets) of the well-established European brands, with a fun factor with which they could not compete. He commissioned artwork from Ken Done and progressively launched variants of Australis products each year. Australis was followed by Australis for Men, which was followed by Love Is Australis. Sales volumes were stable each year, but the growth came from expansion of new product lines.

Jack gestures the size of each market to me. ‘The sunglasses business is this big, the suntan lotion business is this big, the perfume market is this big,’ his hands widening as he describes each market. And finally, he describes his eventual move into cosmetics and widens his hands even further. ‘And that’s why I decided to move into the cosmetics market with Colours of Australis, which is this big.’

With each product launch, Le Specs’ offering broadened. Concurrently to the growth of the distribution business, Jack and his brother Sam would simultaneously expand their footprint of pharmacies which went from 2 stores to 35 while the distribution business was expanding in its own right. This chain of stores would eventually be branded as the MyChemist chain of pharmacies. The hidden benefit of running both a distribution business and a chain of pharmacies was the inside knowledge of which products sold best. The pharmacies owned by Jack were used as testing arenas for different colours of eye shadow, lipstick and makeup – once demand was established, the new line would be sold externally to other pharmacies.

Fine tuning the optimal business model

There are businesses that face more structural headwinds than others. For example, some businesses generate revenue on a per hour basis, which naturally limits how truly scalable the model can be. That is not to say these businesses cannot be profitable and successful, but they face greater challenges and are more vulnerable to adverse market conditions. This was the nature of Jack’s distribution business.

As revenues grew, the working capital required to manufacture and pre-order the sunglasses, suntan lotion, cosmetics and fragrances snowballed. This business model required a large outlay of cash each year, with cash sales received sometimes up to one year later. There would be a build-up of debtors over the year. Compounding this headwind were the banks, who offered working capital financing but required a personal guarantee from Jack and Sam. The larger the business grew, so too did the working capital outlays. It made Jack uncomfortable knowing that he was personally vulnerable to any unforeseen changes in market conditions.

In 1990, twelve years after he started the Le Specs brand, Jack received an offer to sell his business. He and Sam didn’t hesitate to accept, knowing the buyer had much deeper pockets to absorb the working capital requirements. At the time of the sale, Le Specs, Le Tan and Australis business were one of the largest cosmetic distributors in Australia.

The experience gained from the distribution business would serve Jack well in years to come. Jack and Sam had a group of 35 pharmacies in various partnerships and re-focused on growing those to 50 stores. It would be the early formation of what would become Chemist Warehouse – the second phase of Jack’s career and his biggest success. It would become a pharmacy brand that would dominate the Australian market.

***

Part 2 of this feature story on Jack Gance will appear in Morningstar and Firstlinks.

For our other articles on founders, search ‘Founder interview’ in our Knowledge Bank

In Part 2 of my interview, Barry shares his approach to scaling, how he differentiated Count Financial from the plethora of financial services companies, and what he defines as good management.

For readers interested in finding the next Barry Lambert, you must first understand how long-term founders think, as their philosophies are reflected in business strategy, and ultimately flows through to financial performance. In other words, financial performance is only the outcome. To catch founders early, readers need to recognise the hidden engine of the philosophy, strategy and thinking that fuels it all.

Let’s take Count Financial as an example. If my readers were presented with the opportunity to invest in a boutique accounting firm that specialised in tax returns, many would baulk. On the surface, there’s nothing sexy about tax return service providers. But that’s the superficial view. Those readers may not have considered the philosophy and strategy underpinning the business, they may not have looked under the hood to uncover the real source of growth – the engine that allowed Count Financial to morph and evolve their business over a very long period of time. If readers want to find great founder-led investment opportunities, they must first understand how a founder builds a business from the ground up. Results are only the output. The entire picture consists of philosophy, strategy, execution, which leads to results.

Barry Lambert saw it differently than most. Through his business strategies, the initial $90k of capital he invested in the beginning eventually became $373m decades later (a 4000x return). Investors who recognised the nuances of how he ran the business were able to ride his coat tails and participate in the rewards.

The theory of multipliers

In Part 1 we saw how Barry transformed Count from an accounting network into a financial advisory network. Accountants had long-term relationships with their clients, understood their financial goals and had the technical background to provide advice. But back then most accountants weren’t interested in offering investment advice; opening a new business line brought more licencing and compliance obligations – something they didn’t have appetite for as owners of single accounting firms. But therein lay the opportunity for someone like Count Financial. They had a network business that had scale.

As Barry recalls, he saw the opportunity to transition into an investments business and could execute the strategy ahead of others because he was the founder and didn’t have the multiple layers of bureaucracy that prevented many others from pursuing bold untested business models (I’ve written previously about the merits of less bureaucratic companies).

The idea was to obtain investment licencing and offer training to his accounting network, provide all the know-how and investment knowledge to help facilitate them providing investment advice to their clients. In return, Count would take a percentage of all the investment revenues generated by his network. As Barry highlights to me during our interview, he had no interest in servicing individual clients but saw a greater opportunity to instead target accountants and to ‘leverage their client base’, as he says. Count generated revenues as a percentage of total Funds Under Advice across the network, so its growth was scaled across multiple dimensions. First by the number of accounting firms in the network, then by the number of clients within each accounting firm, and each client would have a growing investment portfolio which would also contribute to Count’s bottom line. The model was exponential, not linear.

When I quiz Barry now about how this model was so successful, he attributes it to the ‘multiplier effect’ – the ability for the business to scale revenues by more than one factor, and being the first mover with the truly differentiated service.

Elevation through differentiation

One advantage companies that are still run by their founders have over other companies is that founders have the confidence to be unconventional. Employees worry they’ll get in trouble if they do things differently. Founders don’t. – Paul Graham (Founder of Y Combinator)

As I chat to Barry, he describes a made-up word to me: ‘Surpetition’ he says, in a tone that implies it’s a word I should know. He tells me it’s the name of a book written by Edward De Bono and its concepts stuck with him for decades, and a key ingredient of how he differentiated Count from its competitors.

For Barry to compete with the incumbents on their arena would be like driving into a traffic jam. As he says to me during the interview, ‘the concept of surpetition is you have to elevate yourself to another level so your competitors don’t come looking for you – you’re operating on a different plane altogether’.

Barry aimed to add a new service each year. Starting with his network of accountants, he soon offered investment licensing and training, then progressively expanding into superannuation, savings, leasing and asset finance. He launched software to aid in the efficiency of his network of accountants. At one point Count had the goal of moving into mortgage broking.

The pace at which new services were being launched was fast. The quicker Count could help its network of accountants entangle their customers, the more entrenched they could become in their financial lives. That was how Count differentiated itself from the competition.

A recipe for longevity

The pursuit of growth for any business requires capital expenditure, funded either with internal cashflows or externally through the use of debt or additional equity. Under Barry’s leadership, Count always chose internal cashflows, never debt. Barry recalls in the late 1980’s when he took out a $200,000 working capital facility and discovered the interest rate was 20.5% (in those days interest rates weren’t shown on statements so he had to call up to discover that surprise). Barry paid off the loan and decided from then on he would never take out another loan for the business ever again.

And Count never had to. It was profitable and able to use internal cashflows to fund its growth strategies (I’ve discussed this compounding mindset previously). Unlike his competitors, Barry had a conservative approach to expenses. Competitors would come and go, often bursting onto the scene with big marketing budgets that eventually fizzled out. Barry tells me there was one competitor backed by a large corporate who muscled in with a $2 million marketing budget over 1-2 years. They didn’t last in the end.

A debt-free capital structure makes sense in some environments, but not necessarily in others. Count could use its strong financial foundation as a weapon to outlast its competitors. The strategy proved effective in the financial services environment where market saturation takes time.

Readers interested in these founder profiles can subscribe to the Lumenary newsletter for the latest updates and future publications.

Barry Lambert founded Count Financial in 1980, bootstrapping the business and running it whilst still juggling a full-time job at CBA. The business that started out as a “necessity to pay for three kids and a big mortgage” was eventually sold to CBA for $373 million 31 years later.

In this publication I distil some of Barry’s lessons which apply not only to business, but to life. And with each interview session I delved deeper into his mindset, drawing out the behavioural differences which make founder-led companies such a special hunting ground for investors.

After Hours Tax Services. That was the name first given to Count when it was born in 1980. If ever there was a business name that aptly reflected the inner personality of it’s founder, After Hours Tax Services would be it. Barry oozes an aura of pragmatism and straight talk.

In a deep raspy voice Barry tells me he needed side income and that’s why he started working on tax returns as a side hustle. He explains how he sought approval from his then employer CBA, noting to them there was no conflict of interest, since he was working at head office and had no direct contact with customers, therefore posed no risk to the bank. He was approved, and the next day he placed an ad in the Yellow Pages.

The response from the ad was strong. Because he was busy with his day job and couldn’t travel to service all the customers, he started outsourcing the work to other accountants, taking a skim for each client he referred. That was how Count’s accounting network started in the early days.

As the network and customer base grew, so too did Barry’s income. Barry chuckles as he recalls how after a few years the side gig was making him four times the salary of his full-time job at CBA. He had achieved his original goal – the business was making ample income for him to support his family whilst concurrently developing a career in banking.

So why not keep the side business going while he built his career in banking? What motivated Barry enough to ultimately quit CBA and pursue business full-time?

The answer came down to the very core of Barry’s philosophy in business – do what’s right for the client. And he didn’t see this philosophy at all when he was at CBA. In fact he witnessed the opposite. Back then incentive frameworks were designed to push clients into low-yielding products called Non-Interest Bearing Accounts (NIBA) and with inflation at all time highs in the 1980’s, clients’ wealth were being eroded away in these NIBAs. Yet the banks continued to promote NIBAs. This didn’t sit well with Barry. As he says to me “I’m not particularly religious, but I have a strong sense of right and wrong”.

He voiced his disagreement to higher ups to no avail, and so he eventually left CBA after 18 years to pursue his business full-time, knowing that he was in control of doing the right thing by his clients. This was the fundamental crux of what Count Financial was about, and would motivate Barry for the next three decades. The concept of doing the right thing by the client proved to be a winning formula not only for Count’s corporate persona, but also because it was a genuine commercial advantage that won market share. Clients listened to technical experts (accountants), rather than salespeople with vested interests.

Speed of improvement

Barry’s matter-of-fact approach to business rubbed off on the way Count was run – if improvements made sense, they would be done quickly without bureaucratic red tape. Take for instance licencing. Count was an early adopter of Australian Financial Services (AFS) Licensing for its financial advisors, the philosophy being to remain ahead of regulations, rather than on the back foot. Back then this wasn’t the norm, many companies took a wait-and-see approach when it came to regulatory compliance. There were some of Count’s competitors that were outright complacent – Barry recalls how he raised the need for licencing at a lunch with a Big 4 bank and was told “licencing is for people like you; we don’t need to be licenced”.

Improvement is a necessity of business. Change is inevitable and that was how Barry saw it. As it turns out, he was right.

The speed at which improvements could be made at Count was enabled by its relatively flat hierarchy. Barry remained the brains of the business and all major decisions went through him. There were no convoluted committees and steering groups to contend with. If the strategy made sense, it could be executed much faster than the competition. Case in point – Count converted into a paperless operation over a few weeks, again an early adopter of emails. They lost seven accounting firms in the transition, but as Barry says, it was necessary to keep improving the efficiency of the business. Making a change this bold in any other organisation would have taken years to decide and even more years to implement. For a founder, speed is an advantage.

I can still picture Barry chuckling as he says to me “I don’t mind the banks being a competitor because I know I’ll be 5 years ahead of them”. How true.

Problem solving

Barry points out the subtle difference between speed of execution versus speed of decision-making. Executing quickly doesn’t mean decisions are rushed and ill-considered. Quite the contrary as Barry explains to me. He often took his time with decisions “it [the solution] often doesn’t come to you straight away, you usually have to sit on it a bit”.

There are two main criteria Barry uses to make big decisions:

solve the problem from first principles rather than copying others; benchmarking is a flawed concept

the answer should be simple to manage and not too stressful to implement

It was with this framework that Count morphed itself from an accounting network into a wealth management network. In the 1980’s there were no other hybrid accountant/financial planner firms. As with all great ideas, it always seems so obvious in hindsight; there was no one better placed to provide finance advice than accountants who knew the financial position of their clients intimately.

The solution came about not because Barry copied a competitor, but because he started receiving a lot of calls from wealth advisors who wanted referrals from Count’s network. The problem was these were all salespeople who were motivated by selling investment products, not providing the right advice for clients. Barry disagreed with that. “Clients deserve to receive financial advice from professionals and not salespeople” was how he put it to me. Count applied for its financial advisory licence and started the new service the following year.

Count had carved out a unique position in a competitive field. By not copying others, Barry created a first mover advantage because Count was truly independent and relied on accountants providing tailored financial advice, a clear differentiator from his competitors who appointed salespeople to promote the selling of financial products as though they were selling a pair of shoes.

The unique strategies Barry used to scale Count Financial will be covered in Part 2 of my interview along with how he extended the gap between Count and its competitors, and his thoughts on effective management.

Founders have changed the world and will continue as long as capitalism exists. Our system motivates bright individuals to pursue dreams and build companies that improve human lives, just as trees in a canopy compete vertically for sunlight. For us investors, we need not miss out on these game-changers. We can participate in the rise of these companies alongside their founders, and if the analytical judgement is cast correctly, stand to benefit immensely from their journey.

Are all founder-led companies start ups?

Investing in founder-led companies does not mean venture capital investing – there are over 2,000 listed founder-led companies globally, varying in age, size and industry. Not all founders work on new and shiny products, only a small proportion are start ups. In fact, there are many blue-chip founder-led companies that are not in the technology sector, and these global household giants should resonate with many of my readers: Marriott, Morningstar, Hermes, Walmart and Nike.

What are the risks of founder-led companies?

The pros of investing in founder-led companies are well documented by academics and practitioners alike – Credit Suisse and Bain have quantified a +7% outperformance since 2006. Other studies show multi-decade alpha. In business, skin in the game matters and that is why founders make great business owners and operators.

But not all founders are great. Not all founder-led companies turn out to be the next Amazon. Hence everything in moderation, and why diversification is needed to dampen the volatility of owning just one company. This is where a clear portfolio construction recipe comes in.

I have previously likened portfolios to making a cake in this previous publication here . We select our best ingredients and apply them in the right proportions before baking in an oven at the right temperature. What generates returns is not what has happened, but what will happen. And proportions are crucial.

Instead of baking one cake with all our cake mix and hoping it turns out well, we should divide the cake mix to make many cakes. With each cake we make, risk is reduced. That is the key to a well-balanced portfolio of founder-led companies. The sum of the parts is always greater than the whole, especially when it comes to risk management.

There is an optimal way to diversify and the framework for this process is tied with the concept of vintages.

How to diversify a portfolio of founder-led companies

The least volatile founder-led companies are also usually the oldest. Think Walmart, Hermes and Nike, who have each existed for decades. The advantage of these generational companies is the stability of growth and predictability of dividends. They move like ocean liners, their brands carry inertia that spins off free cash flow consistently. You can rely on these founder-led companies to deliver slow and steady growth to your portfolio. The advantages are not without risk though. Older generational companies can become complacent. Their founders may have already reaped the rewards of their lifetime of efforts and become content with sitting back and relaxing. Their succession planning may not be smooth. The companies themselves may not be built the right way to adapt to changing environments. Ocean liners have a huge turning circle; it becomes impossible to navigate fast-changing conditions when they have only been built to travel in straight lines. I’ve written previously about how up-and-coming companies can lower the risk of a portfolio here.

This is why portfolios should be built to capture the full spectrum of founders from different vintages. You want both ocean liners and speedboats. Younger founders are hungry and motivated. They are free of the shackles imposed by legacy constraints. In this day and age, issues caused by use of outdated technology can prove significant for incumbents – you can observe how difficult it is for banks to transform their systems. It is easier and faster to build from scratch than it is to modify, much like how building a new house is faster than renovating an old building. When the pace of change increases, newcomers have the advantage. Niches open up in fast changing industries, and I’ve previously outlined some of these in this article.

Take for example a company my fund is invested in. It’s a Dutch company called Adyen in the global payments market. They’ve been built with technology from the ground up that allows them to outcompete incumbents. As a result, they have been able to win significant market share in a very short period of time and capture the accelerating change in consumer payment behaviour.

When it comes to founder-led companies, there are pros and cons to both old and young. Having all your eggs in either one or the other would be unwise. Spread your portfolio across founders from all vintages.

You want to build a fleet that encompasses the ocean liners, giving stability and reliability, and mix them with speedboats who can navigate changing environments and adapt with the times. This is what can truly mitigate risk.

Skin in the game – when theory meets practice

A final question and thought for my readers: which of these investment opportunities is inherently riskier over the long term:

Multinational blue-chip where the board has employed a salaried CEO on a 5-year contract; or

A mid-cap company where the founder retains majority ownership, is the CEO and Chair.

The multinational blue-chip has existed for much longer, so its share price is more predictable, less volatile. The mid-cap founder-led company has a much more volatile share price – analysts have a wide variety of opinions regarding its prospects.

But which one is riskier over the long term? Which company would you rather invest in?

The answer depends on your understanding of the difference between risk and volatility. One investment is more volatile but is actually less risky over the long term.

Epicormic buds lie dormant, hiding underneath tree bark waiting for the right conditions to sprout. They serve a regenerative purpose in the overall forest system and flourish when conditions are at their most dire. Bushfires for example, trigger epicormic buds to sprout with extreme heat and the clearing of nearby vegetation. In other words, the emergence of new growth stems from the wreckage of the established.

Just as a botanist studies epicormic growth, I’ve been looking at buds and shoots in a different world. The questions remain the same. Which environments foster this latent growth? Where can I find the most regeneration?

I’ve spent a lot of time investigating these questions in the context of the current investment environment and I’ll outline how I’ve positioned my fund.

Noise, distractions, smoke and epicormic buds

There’s a lot of noise in financial markets. Think back only a few months ago during the Trump presidency. The headlines were volatile and anxiety inducing. We had it all, from a promise to clamp down on big pharma, to the US expulsion of Chinese companies accused of breaching data security, and the US withdrawal from the Paris climate accord. I’ve raised these headlines as examples because as much noise as they created at the time, they have all fizzled out like an old balloon. The world keeps revolving. But feel for Mr. Market, for at the time he was brought to his knees by the amount of anxiety this news had caused him. One can look back now and reassure him everything is ok, but at the time he was in no state.

Today the noise is all to do with interest rates and inflation. Endless predictions about the actions of central bankers and the interpretation of every word spoken at press conferences. The problem with short-termism and quick news is that everyone is focused on it. Everyone has an opinion. It’s a crowded space. It is not where you can get a competitive edge as an investor. Instead, the edge comes from being able to strip away the noise and focus not on the smoke and fire, but seeking out the epicormic buds that are developing underneath. Don’t be like Mr. Market. I’ve written previously about the sources of alpha in this publication.

The most common theme of today

Let me paraphrase today’s rhetoric:

A huge wave of inflation is coming. Bond yields will rise in response, and so too will interest rates. This leads to a revaluation of assets as the time value of money increases the value of predictable cashflows as opposed to the uncertain.

This means companies with predictable cashflows come back into favour (value), as opposed to those with unpredictable future revenues (growth). It’s a matter of perception – interest rates alter how analysts value companies, just like how the sea level changes the impression of a mountain’s height.

The fact remains, a valuable company will remain valuable, just as a mountain remains a mountain. The effectiveness of either strategy, growth or value, is driven by the prevailing market conditions and whichever curries favour. Just like fashion trends, market conditions are becoming increasingly unpredictable.

Growth investors flourished last year as technology companies soared, but if your allocation had been solely to growth, you would be having a rough couple of months of late. The key to a resilient strategy is to remain adaptive. This means having a balanced portfolio that flexes with prevailing conditions without being overly extreme any which way. I’ve touched on the importance of asset allocation in this article.

And this is how I’ve positioned my portfolio.

Structuring a portfolio in today’s environment

Given the inherent uncertainty and whimsical views of the market, there is opportunity to profit from both growth and value when markets flip from one school of thought to the other. With a dual structure, a portfolio remains balanced, there are no big bets and risk is tempered. What I’m seeking is a resilient portfolio that focuses on two types of buds.

Bud 1: Emerging companies selling new products and services

Bud 2: Existing companies experiencing temporary price dislocations but due for a resurgence

This structure captures the rise of both growth and value whichever the direction of sentiment. A 50/50 split at the start, which is then flexed when the opportunities prevail.

When I look for the Bud 1’s, I’m looking for emerging companies that offer a compelling new product or service. They aren’t startups, their product should be new, yet proven with growing demand. The customer base absorbs the new product like a fresh paper towel to a drop of water. It solves a problem the world has struggled with previously and craves for.

When analysing the Bud 2’s, the lens is different – I’m looking for a resurgence or reinvention of an established business. Sentiment surrounding them may be negative and they may be facing a challenging macro environment. I’m looking for headlines that make Mr. Market nauseous. The bigger his overreaction, the better the opportunity.

Growth – the first mover advantage

Delving further into the first type of buds – emerging companies selling new products and services. This is all about capturing long-term possibilities and investing in growth opportunities.

Given today’s market conditions, it’s important to de-risk growth investing given the uncertainty with inflation and interest rates. I mentioned one of the strategies is to stick with proven new products that are already experiencing growing customer demand. Equally important is to find companies facing few competitors. If they’re selling a new product or service, they should be one of the first movers solving a big problem for the world. Again it’s all about de-risking the potential for a margin squeeze if inflation picks up. The safest companies in inflationary environments are those that command monopolistic pricing power.

Some readers may wonder: why not just avoid growth investing altogether? The weakness of this strategy is it assumes you’ll be 100% right about the timing of when interest rates will rise. The all-terrain portfolio seeks to capture gains from any possible direction the market takes, including the next generation of world-changing companies. Sea levels fluctuate with the tide, but mountains will still be mountains.

Value – opportunities lie where there is greatest anxiety

Equally important is the search for the second type of buds – existing companies experiencing temporary price dislocations but due for a resurgence. These are the established businesses that haven’t fully recovered from the pandemic – and there’s plenty of them globally. In Australia we’ve recovered quickly but if you look across Europe, US and Asia, industries such as entertainment, hospitality, drinks, logistics and leisure will explode when their lockdowns abate.

Mr Market ruminates on uncertainty and often winds himself up in knots. Look for areas of greatest anxiety and that’s where you’ll find the greatest value. Value investing is about picking up immediate mispricings and targeting shorter term profits. I cover how investors can determine if the trend is their actual friend in this article. But be prepared when stocks reach full value, you’ll need to offload and recycle the strategy when growth plateaus to normalised rates.

The problem with short-termism and quick news is that everyone is focused on it. Everyone has an opinion. It’s a crowded space. It is not where you can get a competitive edge as an investor. Instead, the edge comes from being able to strip away the noise and focus not on the smoke and fire, but seeking out the epicormic buds that are developing underneath.

Balancing the risk and reward

How the portfolio gels together is equally important as each individual investment. I spend the same amount of time thinking about the correlations between each investment to ensure the all-terrain portfolio spreads volatility. Look far away to Europe and Asia which are on a different recovery trajectory to the US and Australia. As specialists in founder-led companies, I also find European and Asian founders more prudently focused on generating profits rather than pumping revenue metrics, which again tempers the risk.

After any devastation, there will always be new growth. As the world recovers from this one-in-a-century event, pay attention to both the emerging new buds and the recovery of the existing trees. There are two types of gains to be made so make sure your all-terrain portfolio places you well for both.

Happy compounding.

About me

Lawrence Lam is the Managing Director & Founder of Lumenary, a fund that invests in the best founder-led companies in the world. We scour the world looking for unique, overlooked companies in markets and industries on the edge of greatness. We are a different type of global fund – for more articles and information about us, visit https://lumenaryinvest.com

Disclaimer

The material in this article is general information only and does not consider any individual’s investment objectives. All stocks mentioned have been used for illustrative purposes only and do not represent any buy or sell recommendations.

When we think about investing, we always think about buying. We spend enormous amounts of time forecasting the future, distilling vast stores of information into one single click of a green button. But what is commonly overlooked, is the other side of the equation – selling. It remains the poor cousin of buying, yet it shouldn’t be. Selling is as important to investing as braking is to driving. Selling at the right time is just as important as timing on the entry. Yet all too often, investors only know the accelerator and gloss over the analytical framework of selling. In doing so, they give up much of the hard work they have put in to establish the buy thesis.

Why are institutional investors so bad at selling?

It may surprise you to know institutional investors do not have an edge when it comes to selling. Recent researchers[1]studied the outcomes of selling decisions and determined there was substantial underperformance over the long-term. So bad were the selling decisions they even failed to beat a random selling strategy. These weren’t retail investors. The study looked at portfolio managers with an average USD $600 million size. The outcome? They still failed to outperform a simple randomised strategy.

But why are institutions so bad at selling?

Poor selling hurts returns more than you think

Without an analytical framework for selling, investors use mental shortcuts which are susceptible to behavioural biases and lead to inconsistent results. Poor selling can hurt you in two ways. First, you can sell out of a great company too early. The seed of a Californian redwood tree is only a tiny speck yet it has great potential beyond its appearance. Dispose of those seeds and you end up missing out on a giant.

Second, a weakness in your selling process can lead to prolonging a losing investment far too long. Our cognitive biases can shroud our judgement. We can become committed to a previous decision and fail to see how changing circumstances no longer make an investment worthy of our portfolios.

The psychology of selling

Inspecting my own game, I came to realise the importance of a strong short game to complement my long game. By ‘short’ I mean selling stocks you own, not short selling (which is selling what you don’t own). Most fund managers only focus on their long game and disregard the short (I suspect this is also true of their golf). The research[2] supports this. Professional investors are able to outperform through stock selection and buying, but many underperform when it comes to selling decisions.

But why? Buying and selling are simply two sides of the same coin. If one can make good buying decisions, why does it differ so much when it comes to selling?

Use heuristics with caution

Recall earlier I introduced the term ‘mental shortcuts’. In psychology, these are known as heuristics. They’re good for simple decision making, but detrimental when it comes to complex analysis required in investing. Without a system of thought when selling, we gravitate back towards a structureless approach. And this is where it can go wrong for many investors. Even at the institutional level, cognitive biases creep in. Research found the most common being:

The disposition effect: a reluctance towards selling losers, and inclination to selling winners.

Overconfidence: assuming you will make the right decision to sell without any factual analysis.

Narrow bracketing: looking at decisions in isolation without consideration for the broader picture. Analysts who focus on one geographic or sector are most susceptible to this.

From my own experience, I deploy more capital to those investments that I have greater conviction in. The greater weighting reflects my analysis and the velocity which I think returns can be made. This conviction when entering a stock also translates to better selling performance on exit. Another takeaway from the study shows poor selling decisions tie closely with low conviction investing. Just think about those stocks representing the smallest proportion of your portfolio. These are the stocks you are most likely to make bad sell decisions with.

Knee-jerks that hurt

One of the main reasons institutional investors make bad selling decisions is because they react to price movements. All the fundamental analysis done when deciding to buy is not mirrored when they sell. Instead, sell decisions are either automatically triggered via stop losses or to capture recent gains. Either way, basing selling decisions purely on price is what leads to underperformance. To counter a pure price focus, the questions investors should focus on are:

Have business prospects fundamentally changed for the future?

Are customers migrating away from this industry?

Does the company still retain its competitive edge?

It’s that time of year

Following closely behind automated selling strategies are the financial calendar trades which occur when professional fund managers decide to sell for no other reason than to realise taxable losses or crystalise their gains as they massage their financial year end results. Annual bonuses drive selling decisions which are proven to underperform in the long-term. From the portfolio manager’s perspective, it may not matter if they are rewarded for these decisions so long as they achieve their end of financial year KPIs.

Knowing these weaknesses is one thing, mitigating them is another. It is only once these issues become known that addressing them becomes possible.

Incentives that create value

The single hardest and simplest correction for most investors is to align your long-term incentives with your selling strategy. If your investment strategy is long-term and you want to compound your investments, then set up a framework that rewards careful, fundamental analysis before selling. I’ve written about this previously here. The same questions when buying should be applied to selling. Here is where private investors have an in-built advantage over institutions – they innately possess the flexibility and natural incentive to perform over the long-term; ignore the arbitrary financial year end distractions and focus on the real fundamentals.

Institutional managers need to think as if they are the largest investor in their fund.

Investing with conviction matters

Dipping toes in waters is not the optimal way to invest. Concentration leads to outperformance as it encourages deeper analysis. Nothing like a big investment to ward off capriciousness. The benefit isn’t only on the buy side. The research shows selling decisions benefit too when concentration is higher. Invest mindfully and with meaning. Underperformance happens when you’re selling out of a stock you were never that convinced with in the beginning. Easy come, easy go, but you will pay for it when you sell.

Stress and other suboptimal influences

Have business prospects fundamentally changed for the future?

Are customers migrating away from this industry?

Does the company still retain its competitive edge?

The answers to these questions will inform whether you hold or sell.

But as we have seen recently, when you’re facing a 30-40% drop in prices, the stomach will take over the mind. Stress sets in, sometimes even panic. This pressure is even greater for institutions who have to report back to thousands of clients. They become price-reactionary. Heuristics to invade the decision-making process when time is pressured. Evidence points to the most severe underperformance on sales coming after extreme price movements. Institutional investors are susceptible to mental shortcuts as they tend to use stop-losses, automatic rebalancing to benchmark weighting, and auto profit-taking triggers to simplify sell decisions.

Sell because of changes in business prospects, not because of stock price movements, even if you’re under extreme market pressure.

How to use feedback

Institutions spend less time analysing the selling decision. They will meticulously track buying decisions, but they rarely analyse how selling decisions went. A technique I employ to improve selling decisions is to elucidate myself with iterative feedback. Track the results of selling decisions just as you would with buying decisions. Each iteration of feedback informs how a sell decision can be improved for next time. Without it, investors are blind to their own mistakes.

The dangers of commitment bias

Cognitive biases cloud our judgement and none are worse than our feeling of commitment that encourages us to hold onto investments longer than we should. The sell decision is based on logic and business prospects in the future. Waiting for an eventual turnaround is useless if a company’s customer base has fundamentally changed, or if its competitive advantages have been eroded by competition. I have scars to show for this misjudgement. Under-selling can be just as detrimental as over-selling.

The evolution of selling

The evolution of any investor understandably begins with focusing on buying, but sophisticated investors that truly understand when and how to sell, transcend into becoming adaptive investors able to compound wealth in any market condition. Adaptive capital is where you ride each wave as it presents itself. To do that, you need to be skillful at braking, not just accelerating.

Happy compounding.

About me

Lawrence Lam is the Managing Director & Founder of Lumenary, a fund that invests in the best founder-led companies in the world. We scour the world looking for unique, overlooked companies in markets and industries on the edge of greatness. We are a different type of global fund – for more articles and information about us, visit https://lumenaryinvest.com

Disclaimer

The material in this article is general information only and does not consider any individual’s investment objectives. All stocks mentioned have been used for illustrative purposes only and do not represent any buy or sell recommendations.

[1] Akepanidtaworn, Klakow and Di Mascio, Rick and Imas, Alex and Schmidt, Lawrence, Selling Fast and Buying Slow: Heuristics and Trading Performance of Institutional Investors (September 2019). Available at SSRN: https://ssrn.com/abstract=3301277 or http://dx.doi.org/10.2139/ssrn.3301277

This article was first published in Money Management magazine, 8 October 2020

———-

Why do some sports teams remain perennial title favourites, while others seem to consistently languish for decades? If you’re one of the poor souls who finds themselves rooting for the frequent losers, you’ll know the answer isn’t simply ‘our players aren’t up to scratch’. On the other end of the spectrum, the best teams always seem to have an ability to combine mediocre players into a high-performance unit. They seem to be one step ahead of the competition, playing a long game that presciently fills the gaps in their rosters, drafts the best rookies before others spot them, and adapts their capabilities to the evolution of the sport. This is where the behind-the-scenes manoeuvres of the front office management team lead to long-term dominance. These imperceptible strategic decisions go beyond the coach and players, they are macro decisions that create long-term franchises. In investment parlance, asset allocation is exactly those front office decisions you need to make correctly to ensure long-term success. In this publication, we’ll take a deep dive into how two of the world’s best are manoeuvring their portfolio for the future.

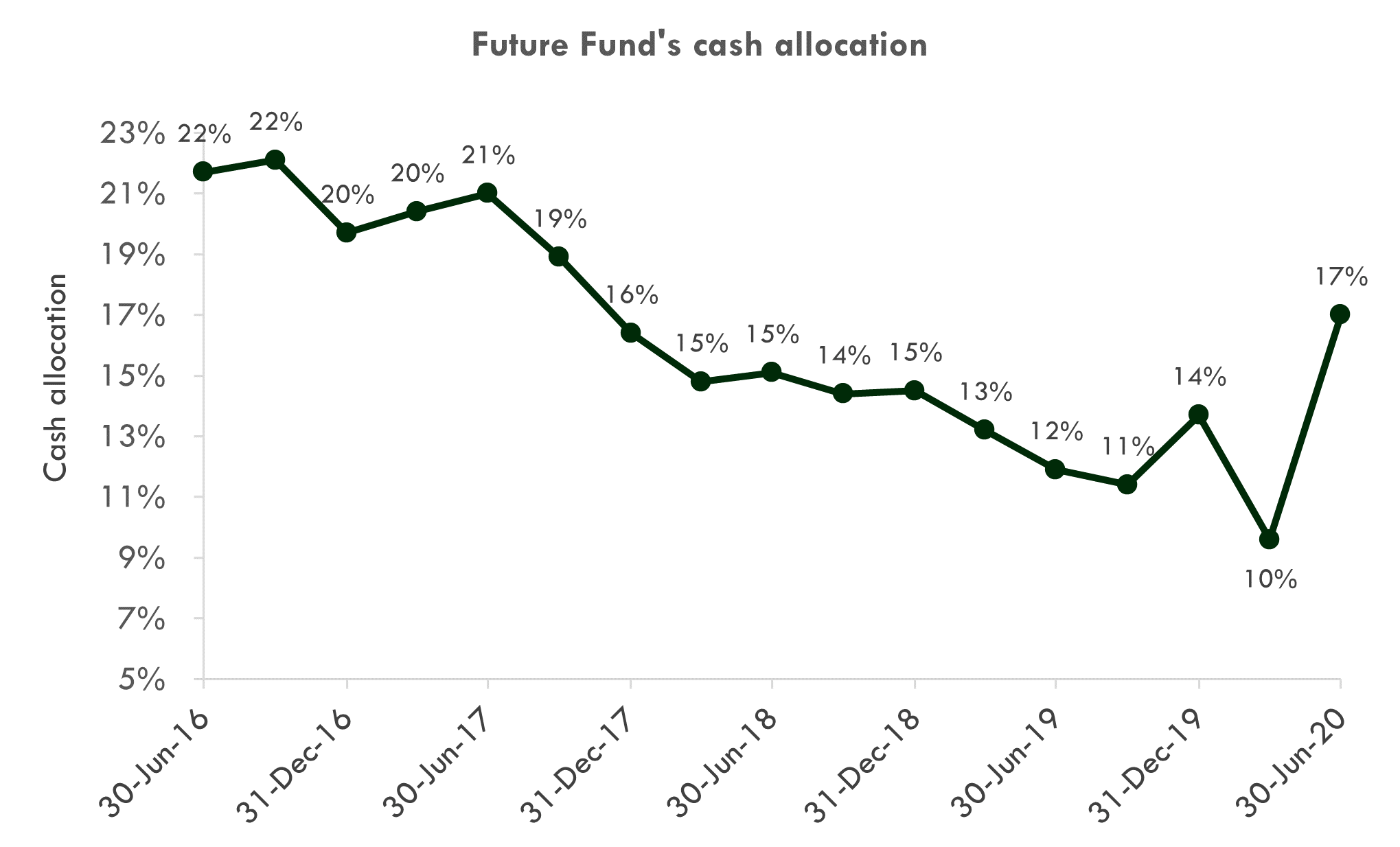

Australia’s Future Fund – anticipate, don’t emulate

A few weeks ago, Future Fund reported their asset allocation on 30 June 2020. Interestingly, they have been cashing in their investments across the board. Their allocation to global equities remains the dominant piece at 27%, but almost all asset classes have decreased across the board. The last time the Future Fund held this level of cash was in September 2017.

Source: Future Fund, Lumenary Analysis

Yes, this does have a little to do with the pandemic, but notice many of the changes were in relation to unlisted assets which take some time to turn over – in other words, many of these liquidations were premeditated and only just came to fruition last quarter. This was far from a spur-of-the-moment reaction to the pandemic.

But just because your cross-town rival makes a change to their team doesn’t mean you should too. Future Fund’s circumstances are far removed from a nimbler private investor and their investment objectives are vastly different. The best sporting teams never emulate the success of others, they create their own success based on independent evaluation. As I delved deeper, the question emerging in my mind was “What can I learn from the intentions of a $161 billion fund, so I can anticipate the next flow of capital, not copy it?”

The bigger they are, the slower they move – but that’s your edge

Delving deeper to uncover the rationale, I found the Future Fund’s CEO had spoken publicly about the portfolio, citing long-term falling interest rates as the cause of asset prices being bid up, which has subsequently led to their cautious view of the world. He went on to explain why he expected headwinds going forward, summarising the year with:

“This year we undertook a material rebalance of the Private Equity portfolio, reducing some of our exposure to international growth and buyout managers following a period of very strong performance. We also completed the sale of other unlisted assets including Gatwick Airport. We deployed some of that capital into new infrastructure themes including fibre and data centres, in Australia and offshore.”

Readers who only skimmed the negative headline would be tempted to cash in the chips and stash money under the pillows. Tempting as it is, I would caution against that. Near-zero rates are fine to accept over the short-term, but a 1% return on cash will destroy wealth over the long-term.