Lawrence Lam sat down recently with Owen Raszkiewicz from the Australian Investors Podcast to discuss living with an entrepreneurial father, investment banking, inequality, valuation, turnarounds and, of course, the founder’s spirit.

Thanks to Owen and Rask Australia. If you enjoyed the podcast, we encourage you all to subscribe to the Australian Investors Podcast.

Lawrence Lam is the Managing Director & Founder of Lumenary, a fund that uncovers the best founder-led companies in the world. We invest in unique, overlooked companies in markets and industries beyond most managers’ reach. We are a different type of global fund – for more articles and information about us, visit www.lumenaryinvest.com

It’s ironic I’m writing my first wire to outline techniques you can use to beat professional fund managers. The fact is, most people assume that professional fund managers have an informational edge over everyday investors. This isn’t true.

These days public information is so widely available and accessible that seeking out detailed information on any listed company isn’t that hard.

Some think fundies have access to meet with company management which gives them an additional informational advantage. This is true only to an extent. The edge is in the ability of fundies to eyeball CEOs and get a sense of the qualitative aspects imperative to a successful business, like culture. But that aside, from an information perspective, these days transcripts of analyst calls can be easily found online. Even if there are meetings, CEOs will always tow the company line and tell fundies what the market already knows.

The only other advantage fundies have isn’t informational. It’s time. They have time to dig out the information because it’s their full time job. But you’ll be pleased to know that there is a finite set of information available. Just because they spend 10 times more hours researching a company doesn’t necessarily mean they have 10 times the advantage over you. There’s only so much relevant information available. At the end of the day, one person still has to synthesise it all and make a call.

As long as you dedicate the appropriate time to turning over the rocks, you can do just as well as us fundies.

Assuming you have the time and patience to do this, here are 3 ways you can beat the fundies at their own game:

1. Ignore the noise and seek out the true source of information

Focus on facts first. Don’t get distracted by macro themes and economic forecasts. Forecasts and thematic investing make for great newspaper reading, but they aren’t factual. It’s based ultimately on others’ opinions. The closer you can get to the true source of information, the better quality information you’ll have to make decisions. You are investing in stocks after all, not economies. And if you look hard enough, you can always find companies that will grow through all types of economic environments.

So instead of reading others’ opinions, your time is better spent understanding a company. What are its business lines? What products do they offer? Who are their customers? What advantage do they have over their competitors? You can find this all online. Start with the current annual report. Then go back historically to see if management have delivered on its original plans. Management presentations, substantial shareholders lists, remuneration and KPI information should all be available on a company’s website. If you find the details about the firm’s activities too complicated, you should move on to the next company.

Social media platforms can be a great source of customer information. Check feedback from customers. How do staff feel working for the company? This information isn’t hard to find. It’s a matter of dedicating the time to it. Spend more time with the true source of information and less time on others’ opinions.

2. Fish in under-fished ponds

Fundies face many structural constraints that you don’t. Larger fund managers are incentivised to spend more time managing the risk of their business, rather than their portfolio. They end up reverting to herd mentality. You can see this when fund managers hold the same stocks, in the same markets.

As a private investor, you don’t face these same constraints. You have the freedom to search in other sectors/markets. You don’t have to find sexy stocks. Boring stocks can be just as profitable. Notice the latest fad and and start your search in the opposite direction. Find companies that have a small public share float. These are founder-led companies where the owners still own a significant portion of the shares. Large fund managers must deploy their capital and companies with small public share floats just won’t capture their attention.

Your advantage is entering into an under-researched trade so you can maximise your chances of finding a good company at a reasonable price. For Australian investors, it’s very easy to get the full list of companies on the ASX sorted by industry on the ASX website. The significant shareholders list is provided in every annual report.

Besides from searching based on sectors, you can look for opportunities in other international markets. Start with markets that others aren’t talking about. There are many free and paid online tools that you can use to find solid companies in these markets. Most allow you to apply a filter that you can use to research further and narrow down your choices to just a few. Take advantage of these little-known companies with less analyst coverage. As the company lays down its promising business expansion plan, you could be in the privileged position of paying the undervalued price before it makes its ultimate positive earnings announcement. Thus, you’ll beat the fundies who will have to deal with a crowded market later on.

3. Focus on quality, not quantity

Fund managers have a business to run as well as a portfolio to manage. Their priority is to spend time marketing to increase the size of their fund and therefore fee income. As they become larger, they are forced to deploy more money in the stock market. Inevitably they can’t spend too much time analysing any one company. Instead they start with the market index and tilt according to which sectors they think will do well. This leads to bloated portfolios that correlate highly with the index. This approach to investing won’t give you significant outperformance – it will give you average returns.

Since you don’t have these constraints, take your time to seek true quality in companies. Start from the ground up and focus on quality over quantity. A concentrated portfolio of solid companies you know intimately will perform better than a scatter-gun portfolio of thousands of stocks you haven’t spent much time understanding.

Concluding remarks

To overtake a car, you can’t drive in the same lane. Don’t assume that fund managers have a huge advantage over you. In fact, they face many structural constraints that you don’t. Choose a different but wiser approach to investing in the stock market and you can beat the fundies. Rely less on hearsay and develop a culture of getting factual information directly from the reliable source. Analyse all the information at hand and focus on quality over quantity. Be patient and be willing to invest in non-mainstream brand name companies. If you approach investing the same way as everyone else, you’ll get the same outcome as everyone else. Happy compounding.

Globalisation will fail if wealth gap between rich and poor is not addressed fairly.

CEOs and managers with long term outlook produce far superior businesses over the long term.

Last week I attended the 2017 AFR Business Summit held in Sydney over two days. An extensive roster of Australia’s most successful business people, politicians and entrepreneurs were invited to speak and discuss the future of Australia.

Many themes were discussed over the two day summit and the speakers I found most insightful were:

Anthony Pratt

Anthony Pratt (Executive Chairman, Visy Industries) – emphasised the importance of growing businesses organically over the long term. Growing businesses from within its own existing circle of competency whilst avoiding growth by over extending into industries or locations unrelated to the current business.

Christian Majgaard

Christian Majgaard (former Head of Global Brand & Business Development, Lego) – grow businesses that focus on the customers/clients needs.

Tim Sims

Tim Sims (second from right: Managing Director, Pacific Equity Partners) – bonuses and other short term incentives for CEOs and managers ineffective. CEOs and managers will aim to set lower targets with the view to exceeding them and maximising their bonus.

Malcolm Turnbull

Malcolm Turnbull (Prime Minister of Australia) – increasing international competition requires Australia to review its company tax rate whilst ensuring globalisation and free trade leave all Australians better off.

It was encouraging to hear these prominent speakers recognise the importance of wealth distribution. Significant time was spent discussing ways of ensuring the positive economic effects of globalisation were properly distributed to those contributing to Australia’s success. Increasing wages and the role of government in redistributing income were heavily emphasised. In my view, it is imperative that business and government seek to address effective wealth distribution – protectionism and closing trade flows is not a viable alternative long term solution.

Disproportionate CEO and senior executive remuneration has also contributed to overall public discontent. In my opinion, this topic must be addressed on a case-by-case basis. Discussion at a generalist level does not adequate address the performance versus salary of each individual CEO.

As an investment manager, the importance of CEO remuneration is relevant to the long term performance and growth of the business – so it matters greatly. The objective of incentives is to align the CEO’s pay packet with those of the investors. In theory, the use of bonuses seems reasonable. In practice, however, they are ineffective. CEO’s will inevitably ‘manage expectations’ of the board by setting their performance targets lower to enable higher outperformance of annual targets. The focus becomes a game of short term expectations management rather than long term business growth.

For an investment manager, it is important to recognise true ownership – we have found that businesses with long term heart keep growing and become more profitable over time.

The debate between the merits of active versus passive investing needn’t be one. These are just tools in toolkit that every investor should use depending on the investing environment.

The wager

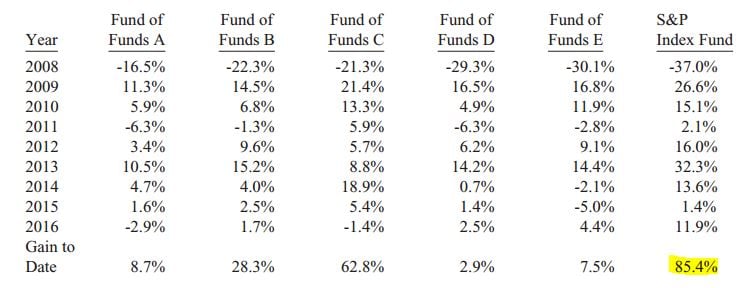

In his most recent 2016 letter to shareholders released last weekend, Warren Buffett described a bet which he had with a hedge fund manager. Commencing in 2008 and now in its 9th year, Warren Buffett wagered that over a 10 year period, a passive index fund invested purely in the S&P 500 Index would outperform a collection of five hedge funds to be selected by an investment professional.

Buffett’s thesis was this – actively managed hedge funds, whilst charging higher fees for investment expertise, could not outperform a passively managed index fund with low fees. The result? With one year to run on the wager, the annual return of the index fund is 7.1% pa and the collection of five hedge funds are returning 2.2% pa. So the lesson it appears, besides from never betting against Warren Buffett, is that every investor should simply invest in index funds.

9 years into Buffett’s wager, here are the results from his annual letter

But I proffer a slightly different argument. Investors should treat active and passive investing as weapons in their arsenal to be used under different investing circumstances. We should not be constrained by the dogma defining us as being a strictly active or strictly passive investor.

A different angle from the Australian perspective

Buffett’s bet should be taken into context. First, his bet is focused on the US stock market. The S&P 500 Index is a collection of the 500 largest companies in America – a truly wide collection of businesses in different industries reflecting the diverse American economy. Of course, Australians can invest in the S&P 500 Index, but from a practical perspective, there would be an implicit foreign exchange exposure distorting the true stock-only returns of the index. The performance would not be an apples for apples comparison. So instead, which indices would a passively minded Australian investor consider? The two possible considerations would be the ASX 300 Index or the All Ordinaries Index.

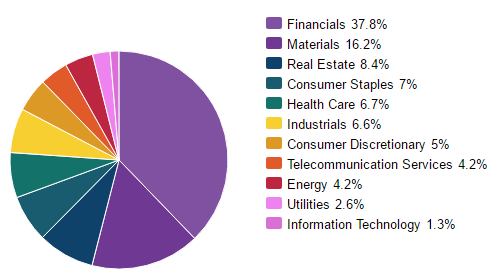

However we know that the Australian stock market is heavily dominated by the big 4 banks and mining/materials companies. This is the nature of the Australian economy. As shown in the 2 comparison charts below, a passive investor in the ASX 300 is not very passive at all. They are investing over half of their funds in the banking and mining/materials industries.

Source: S&P Dow Jones Indices as at 2 March 2017

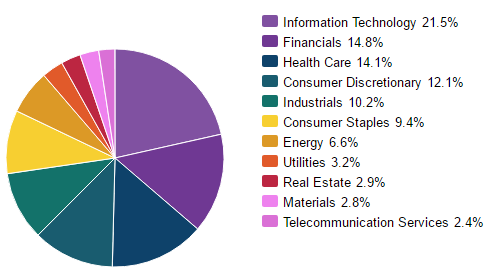

Compare this to the S&P 500 index which is much more diversified. The chart below shows that the American passive investor is truly passive and diversified across many sectors. They are not overweight or underweight in any industry.

Source: S&P Dow Jones Indices as at 2 March 2017

Second, Buffett’s bet commenced in 2008 and is due to finish in 2018 – an unprecedented bull market following the extensive downturn of the Global Financial Crisis. The overall stock market has recovered strongly over this decade. The rising tide has lifted all boats. It is much harder to separate active stock pickers from the overall market if all stocks have rebounded strongly following the GFC. During market downturns is where the great stock pickers are able to separate themselves from the rest of the market.

Why every investor should combine active and passive investing

Instead of defining ourselves as strictly active or strictly passive, we advocate the use of both approaches depending on the environment. From our perspective, we observe that the businesses we would like to purchase are currently overpriced. As such, in this environment, we prefer to allocate our funds to a more passive investing approach. This allows us to temporarily ride the upward tide with the rest of the market. As the tide recedes, we shift towards active stock picking. Our allocation towards purchasing specific businesses increases as we see opportunities arise in the market during a downturn. We have found this approach to be flexible and profitable. It does not tie us down to any strict doctrine but instead allows us to benefit from the best of both worlds.