The debate between the merits of active versus passive investing needn’t be one. These are just tools in toolkit that every investor should use depending on the investing environment.

The wager

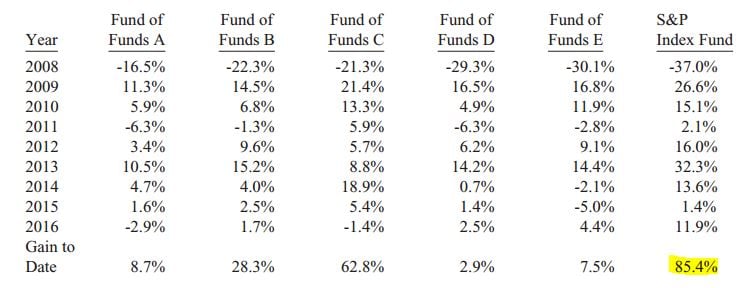

In his most recent 2016 letter to shareholders released last weekend, Warren Buffett described a bet which he had with a hedge fund manager. Commencing in 2008 and now in its 9th year, Warren Buffett wagered that over a 10 year period, a passive index fund invested purely in the S&P 500 Index would outperform a collection of five hedge funds to be selected by an investment professional.

Buffett’s thesis was this – actively managed hedge funds, whilst charging higher fees for investment expertise, could not outperform a passively managed index fund with low fees. The result? With one year to run on the wager, the annual return of the index fund is 7.1% pa and the collection of five hedge funds are returning 2.2% pa. So the lesson it appears, besides from never betting against Warren Buffett, is that every investor should simply invest in index funds.

9 years into Buffett’s wager, here are the results from his annual letter

But I proffer a slightly different argument. Investors should treat active and passive investing as weapons in their arsenal to be used under different investing circumstances. We should not be constrained by the dogma defining us as being a strictly active or strictly passive investor.

A different angle from the Australian perspective

Buffett’s bet should be taken into context. First, his bet is focused on the US stock market. The S&P 500 Index is a collection of the 500 largest companies in America – a truly wide collection of businesses in different industries reflecting the diverse American economy. Of course, Australians can invest in the S&P 500 Index, but from a practical perspective, there would be an implicit foreign exchange exposure distorting the true stock-only returns of the index. The performance would not be an apples for apples comparison. So instead, which indices would a passively minded Australian investor consider? The two possible considerations would be the ASX 300 Index or the All Ordinaries Index.

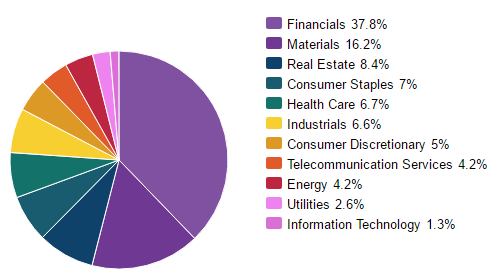

However we know that the Australian stock market is heavily dominated by the big 4 banks and mining/materials companies. This is the nature of the Australian economy. As shown in the 2 comparison charts below, a passive investor in the ASX 300 is not very passive at all. They are investing over half of their funds in the banking and mining/materials industries.

Source: S&P Dow Jones Indices as at 2 March 2017

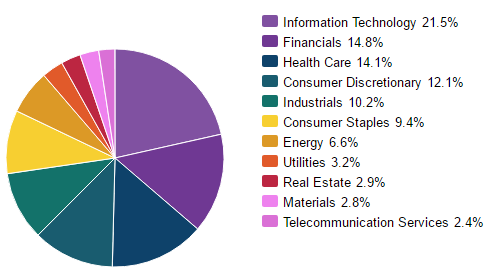

Compare this to the S&P 500 index which is much more diversified. The chart below shows that the American passive investor is truly passive and diversified across many sectors. They are not overweight or underweight in any industry.

Source: S&P Dow Jones Indices as at 2 March 2017

Second, Buffett’s bet commenced in 2008 and is due to finish in 2018 – an unprecedented bull market following the extensive downturn of the Global Financial Crisis. The overall stock market has recovered strongly over this decade. The rising tide has lifted all boats. It is much harder to separate active stock pickers from the overall market if all stocks have rebounded strongly following the GFC. During market downturns is where the great stock pickers are able to separate themselves from the rest of the market.

Why every investor should combine active and passive investing

Instead of defining ourselves as strictly active or strictly passive, we advocate the use of both approaches depending on the environment. From our perspective, we observe that the businesses we would like to purchase are currently overpriced. As such, in this environment, we prefer to allocate our funds to a more passive investing approach. This allows us to temporarily ride the upward tide with the rest of the market. As the tide recedes, we shift towards active stock picking. Our allocation towards purchasing specific businesses increases as we see opportunities arise in the market during a downturn. We have found this approach to be flexible and profitable. It does not tie us down to any strict doctrine but instead allows us to benefit from the best of both worlds.