This article was published in Money Management 7 May 2018

ESG is critical to sustainable outperformance, but where should we focus our research efforts and what are some practical ways to profit from companies with good governance?

______

The relationship between ESG and investment returns is a well-studied area. In this article I won’t be rehashing the detail of the research, which, by the way, show a positive link between ESG factors and financial outperformance of companies. Instead, I’ll be discussing the most important factor, governance. This isn’t a theoretical exercise, it’s an exercise in finding factors that lead to lower risk and higher return companies.

Do ESG factors actually lead to outperformance?

In short, yes. There have been many academic studies in this area and 89% of these studies show a strong correlation of companies that demonstrate high ESG ratings and financial outperformance over the medium to long term (3 to 10 years). Deutsche Bank’s paper “Sustainable Investing: Establishing Long-Term Value and Performance” is a comprehensive summary of all studies conducted in this area, conclusively demonstrating that ESG is not only a good measure of the ethical and moral behaviour of a company, but is critical to the long-term profitability of all companies.

Why are companies with high ESG scores outperforming? The findings show that these companies have a stronger reputation, have higher client satisfaction ratings, are more long-term oriented and this virtuous cycle drives continual financial outperformance.

In addition, 100% of these studies found that these ESG companies have access to lower cost of financing. They can borrow at a lower rate from both debt and equity funding sources. Their sustainable approach to business buys them greater freedom and trust from the funding market. The funding market views these companies as lower risk and therefore affords them a lower cost of funding.

ESG is not an exercise in philosophical values. It is a key factor in the long term financial success of companies. For any investor, this represents an attractive and sustainable investment opportunity.

Environmental, Social or Governance – which factor matters most?

All three factors are quite distinct from each other but the factor that is most correlated to outperformance is governance. Academic studies have defined good governance as having a board structure that is transparent to shareholders, having low CEO turnover, having a strong link between performance of management and employees, having a strong commitment to shareholder protection, strong legal protection for investors and transparency of shareholder disclosures.

In a Quarterly Journal of Economics study, Gompers, Ishii & Metrick’s paper “Corporate governance and equity prices” showed an 8.5% per annum outperformance based on an investment strategy that bought firms with a high governance rating and sold firms with a low rating over the period from 1990 to 1999.

From a practical point of view, since governance is the foundation of how all company decisions are made, a strong culture of governance has a flow on effect to a company’s attitude towards environmental and social factors. The G is the primary factor which leads to good decisions about the E and the S.

A different take on good governance

To summarise, ESG leads to outperformance. Of the E, S and the G, good governance is the most important factor. For investors, the pond of companies with good governance is where one should focus on casting a wide net in. All else equal, this is where the greatest probability of profitability will lie.

So where are these companies with good governance? Previous academic studies have focused on identifying the traits of good governance. These are the proof points of good governance, but they aren’t the underlying cause. Good governance is a fluid concept that can be achieved in many ways. The same measurement of good governance cannot be applied across all companies. It depends on a company’s industry, size, shareholder base and competitive environment – there is no ‘one size fits all’ definition. Ultimately, good governance is having alignment between shareholders and management. This leads to sound business decisions and the proof of this is profit.

So rather than looking for the symptoms of good governance, we should be looking for the diagnosis. It is the cultural DNA of any business that drives its neural network – this is the basis for good governance. From my experience, I have found one key factor common in companies with good governance. The key factor is the influence of its founder. We’re more likely to find companies with good governance if the founder or their family remain influential over the business. This may be in the form of board directorships, management positions, equity holdings or all of the above.

As we review the traits of good governance, we find that founder-led businesses are well placed given their unique cultural DNA.

Transparency to shareholders – shareholders, management and the board may be the same people. Often being a a key shareholder, the founder’s representation at board level guarantees a strong level of alignment between owners of the business and its key decision-makers. Whilst independent representation is important, too much independence dilutes the cultural DNA. Independent input must be encouraged, but final decisions are still made by the founder.

Low CEO turnover – founders or their family may still be involved in managing the company. The CEO, and board of directors may not be the same person, but if they are from the same family then this usually gives a greater level of management stability.

Strong commitment to shareholder protection – founders have skin in the game. The founder’s long-term financial interests are aligned with shareholders. Alignment is strong if founder-led companies have demonstrated long-term profitability and have held equity over multiple generations. The risk of unfair treatment of minority shareholders is minimised because founders are aligned to shareholders.

The path to investment profit

Today, a large spectrum of founder-led businesses exists. They can range from small tech-startups through to generational companies in very traditional industries. In fact 5 of the world’s largest 8 companies are founder-led. The list includes Alphabet, Facebook, Berkshire Hathaway, Alibaba and Amazon. Globally, there are thousands of companies in the founder-led universe to choose from.

Credit Suisse Top 20 family-owned companies by market cap

Source: Datastream, Credit Suisse Research.

Some will argue that a few founder-led businesses have bad standards of corporate governance and lack transparency. But this may be true of all companies. There are good and bad businesses of all types. Importantly, what is the definition of corporate governance? Are we measuring corporate governance according to a rigid scorecard system, or are we measuring corporate governance based on what truly drives each company? Are we applying a standardised set of traits which don’t account for the unique characteristic of each company? The answer is that traditional ESG scorecard measurements are not a good indicator of good governance because governance is much harder to quantify than environmental and social factors.

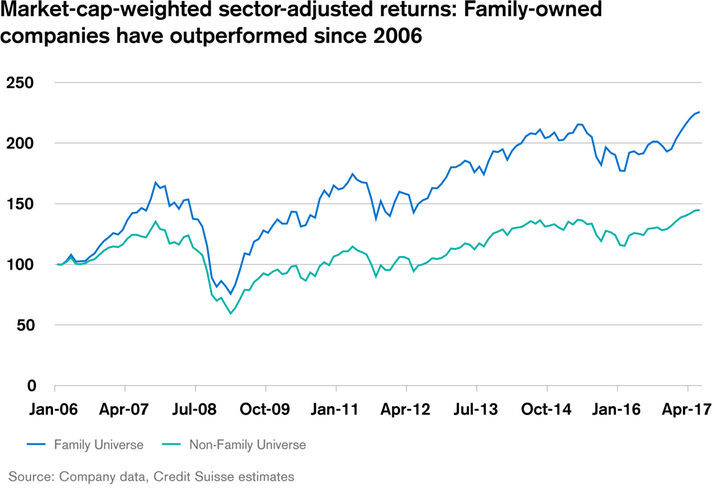

In findings published by Credit Suisse (“The CS Family 1000” report), companies where founders or their family with at least 20% influence via shareholding or voting rights outperformed their peers by 4% per annum.

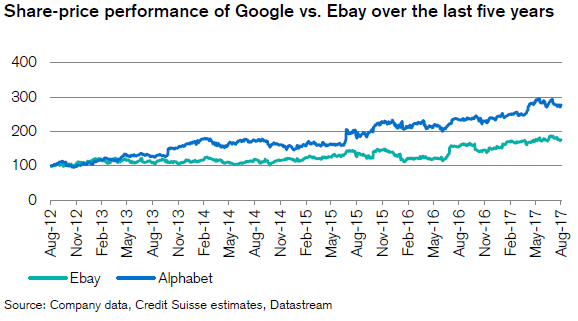

Moreover, they found that although governance scorecard ratings were weaker (only slightly weaker) in founder-led companies, it didn’t matter because the template scorecard measurement was not a good predictor of outperformance – in theory, founder-led companies should be performing badly, but in practice, this wasn’t the case. For example, Google’s scorecard is weak because it does not disclose how its executives are rewarded. However Ebay does, and thus scores higher than Google. But the textbook measurement doesn’t address the underlying cause. Google has performed much better than Ebay not because of it’s scorecard rating, but because it is founder-led.

Governance is a key driver for investment profits, but as an investor, look beyond the traditional rigid definition of good governance and seek out the underlying driver. I have found that founder-led companies the ideal place to start in the search for outperformance.

At the time of writing, Lumenary was not an investor in any of the stocks mentioned.